Copyright 2006 -

HUD has a good booklet on line with tips on how to avoid foreclosure. But what if you’re beyond that point and already into foreclosure? An, why should you be concerned about someone else’s foreclosure, after all it’s not your problem, right?

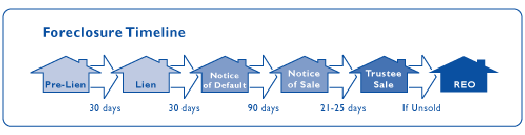

Here is a quick and very brief overview of Michigan’s Foreclosure Laws taken from one of the Webs sites that specialize in that niche.

If the mortgage did not have the power of sale clause, the foreclosure must take place in the courts.

If you’ve been foreclosed, you should read this advice from the IRS about the potential tax consequences

Here are some of the companies or groups that might be on the up-

For senior citizens facing foreclosure

|

|

Hopefully the section above has scared you. It should! You do not want to get to the foreclosure stage. Losing a house to foreclosure can stay on your credit history for up to 12 years and is actually worse than a bankruptcy. Before you get to that stage, let me come in and see if I can help. If you have received a delinquency notice from your lender, the time to act is now, before they get too far into the foreclosure process. |

|

The time before the sheriff's sale of the property is the best time to try to still sell the property and get completely out from under the debt. It’s a time when you need al the help you can get. Give me a call and let us get involved on your behalf. I’ll work on your behalf with the lender to set a fair market price for the house that is acceptable to them and likely to get the house sold. It’s called a short sale because the sale price is “short” of the amount owed, so the lender has to agree to take the deal. Many lenders would rather try to get the property sold at that time, rather than go all the way through the foreclosure process. Short sales are not for the faint of heart, either on the sell or buy side. Go to

my Short sale Web site - | |